TERRY L BURSKY

619.417.5645

REALTOR®

C21 AWARD DRE 01754681

www.TerryBurskyRealtor.com

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^^

^^^^^^^^^^^^^^^^^^^^

Mortgage interest rates have risen by more than half of a point since the beginning of the year, and many assume that if mortgage rates rise, home values will fall. History, however, has shown this not to be true.

Where are home values today compared to the beginning of the year?

While rates have been rising, so have home values. Here are the most recent monthly price increases reported in the Home Price Insights Report from CoreLogic:

Not only did prices continue to appreciate, the level of appreciation accelerated over the first quarter. CoreLogic believes that home prices will increase by 5.2% over the next twelve months.

How can prices rise while mortgage rates increase?

Freddie Mac explained in a recent Insight Report:

Bottom Line

If you are thinking about moving up to your dream home, waiting until later this year and hoping for prices to fall may not be a good strategy.

|

So, you’ve decided to sell your house. You’ve hired a real estate professional to help you through the entire process, and they have asked you what level of access you want to provide to your potential buyers.

There are four elements to a quality listing. At the top of the list is Access, followed by Condition, Financing, and Price. There are many levels of access that you can provide to your agent so that he or she can show your home.

Here are five levels of access that you can give to buyers, along with a brief description:

|

With home prices rising again this year, some are concerned that we may be repeating the 2006 housing bubble that caused families so much pain when it collapsed. Today’s market is quite different than the bubble market of twelve years ago. There are four key metrics that explain why:

1. HOME PRICES

There is no doubt that home prices have reached 2006 levels in many markets across the country. However, after more than a decade, home prices should be much higher based on inflation alone.

Frank Nothaft is the Chief Economist for CoreLogic (which compiles some of the best data on past, current, and future home prices). Nothaft recently explained:

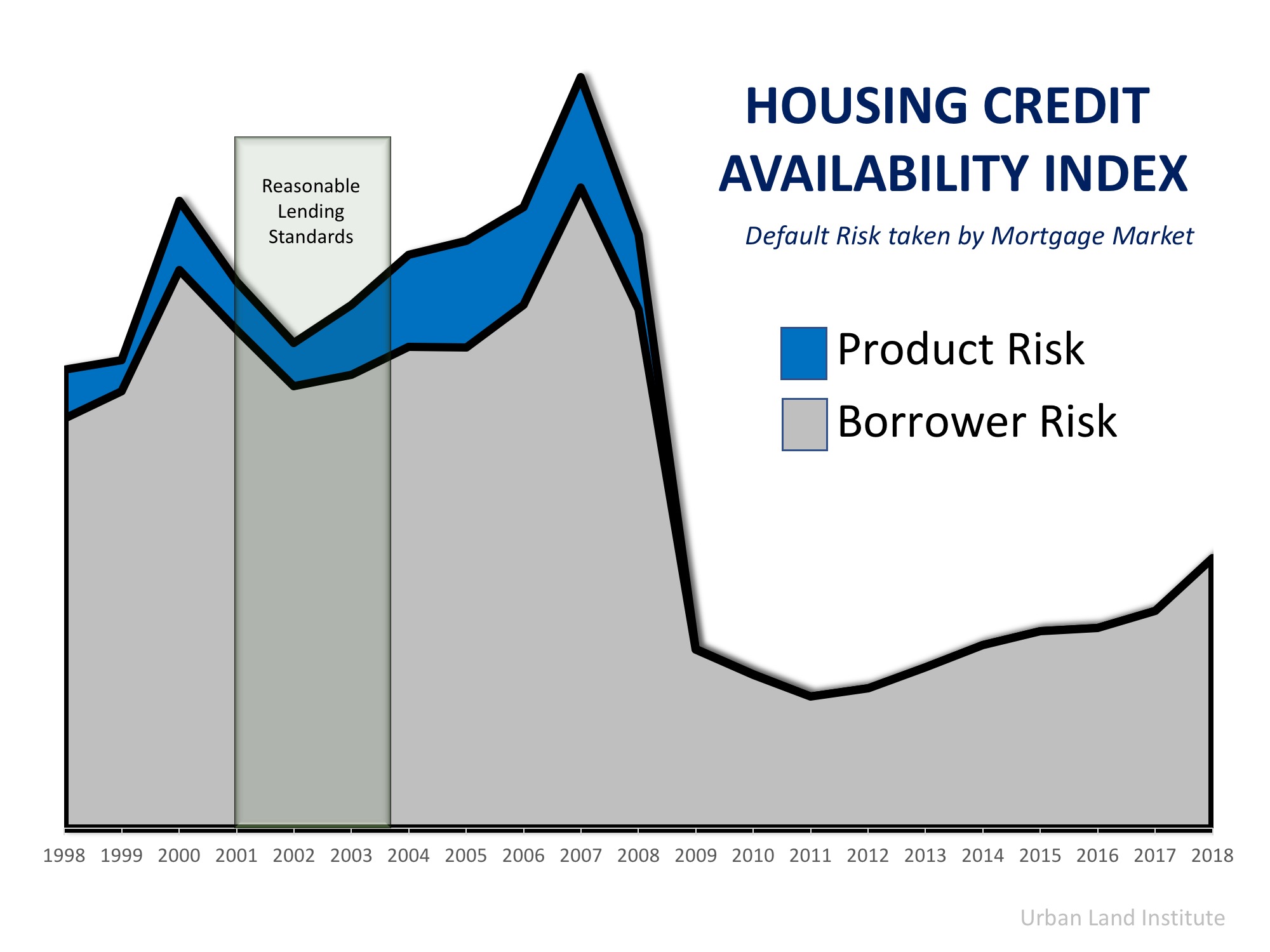

2. MORTGAGE STANDARDS

Some are concerned that banks are once again easing lending standards to a level similar to the one that helped create the last housing bubble. However, there is proof that today’s standards are nowhere near as lenient as they were leading up to the crash.

The Urban Institute’s Housing Finance Policy Center issues a Housing Credit Availability Index (HCAI). According to the Urban Institute:

The graph below reveals that standards today are much tighter on a borrower’s credit situation and have all but eliminated the riskiest loan products.

3. MORTGAGE DEBT

Back in 2006, many homeowners mistakenly used their homes as ATMs by withdrawing their equity and spending it with no concern for the ramifications. They overloaded themselves with mortgage debt that they couldn’t (or wouldn’t) repay when prices crashed. That is not occurring today.

The best indicator of mortgage debt is the Federal Reserve Board’s household Debt Service Ratio for mortgages, which calculates mortgage debt as a percentage of disposable personal income.

At the height of the bubble market a decade ago, the ratio stood at 7.21%. That meant over 7% of disposable personal income was being spent on mortgage payments. Today, the ratio stands at 4.48% – the lowest level in 38 years!

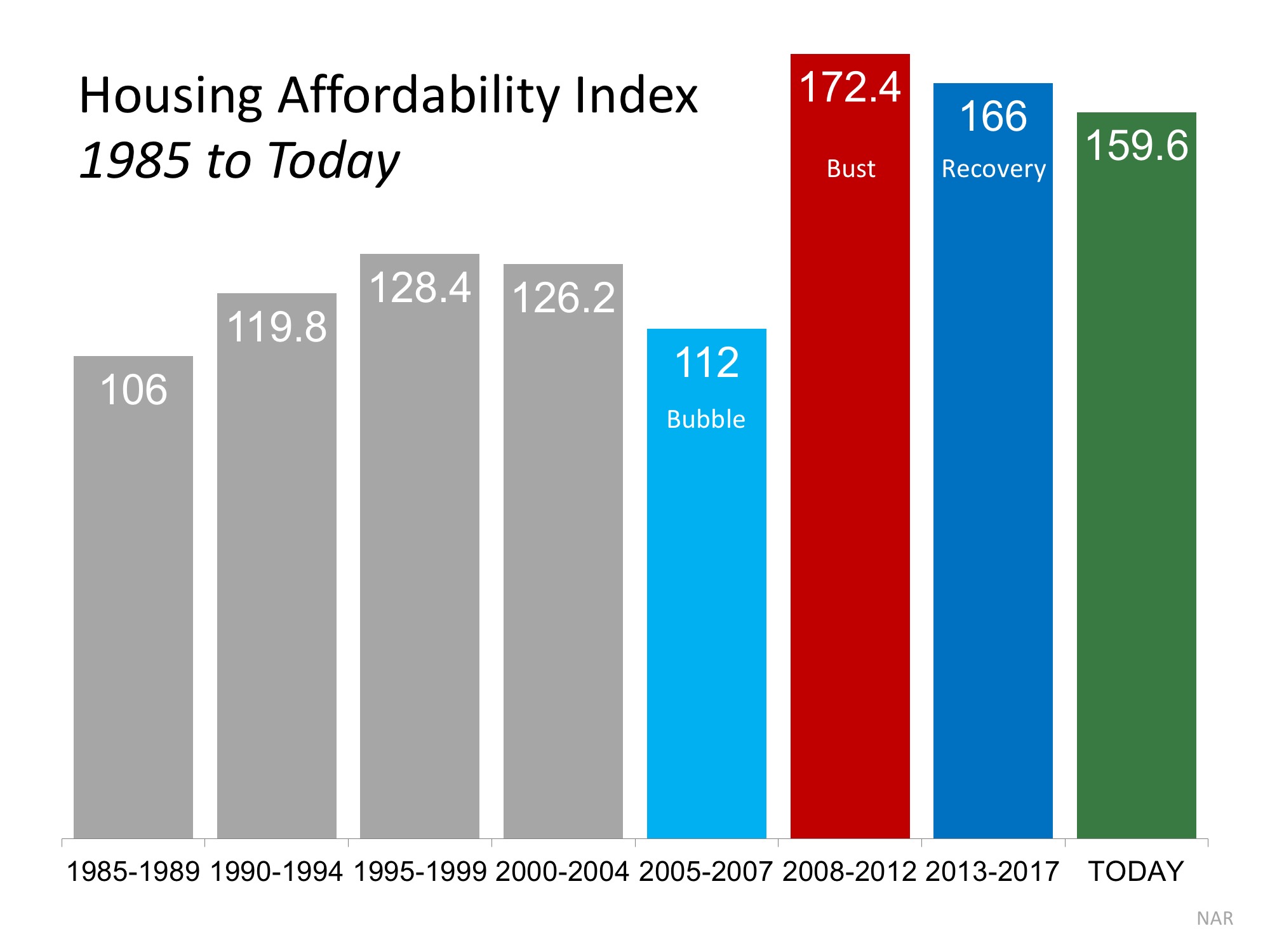

4. HOUSING AFFORDABILITY

With both house prices and mortgage rates on the rise, there is concern that many buyers may no longer be able to afford a home. However, when we look at the Housing Affordability Index released by the National Association of Realtors, homes are more affordable now than at any other time since 1985 (except for when prices crashed after the bubble popped in 2008).

Bottom Line

After using four key housing metrics to compare today to 2006, we can see that the current market is not anything like the bubble market.

|

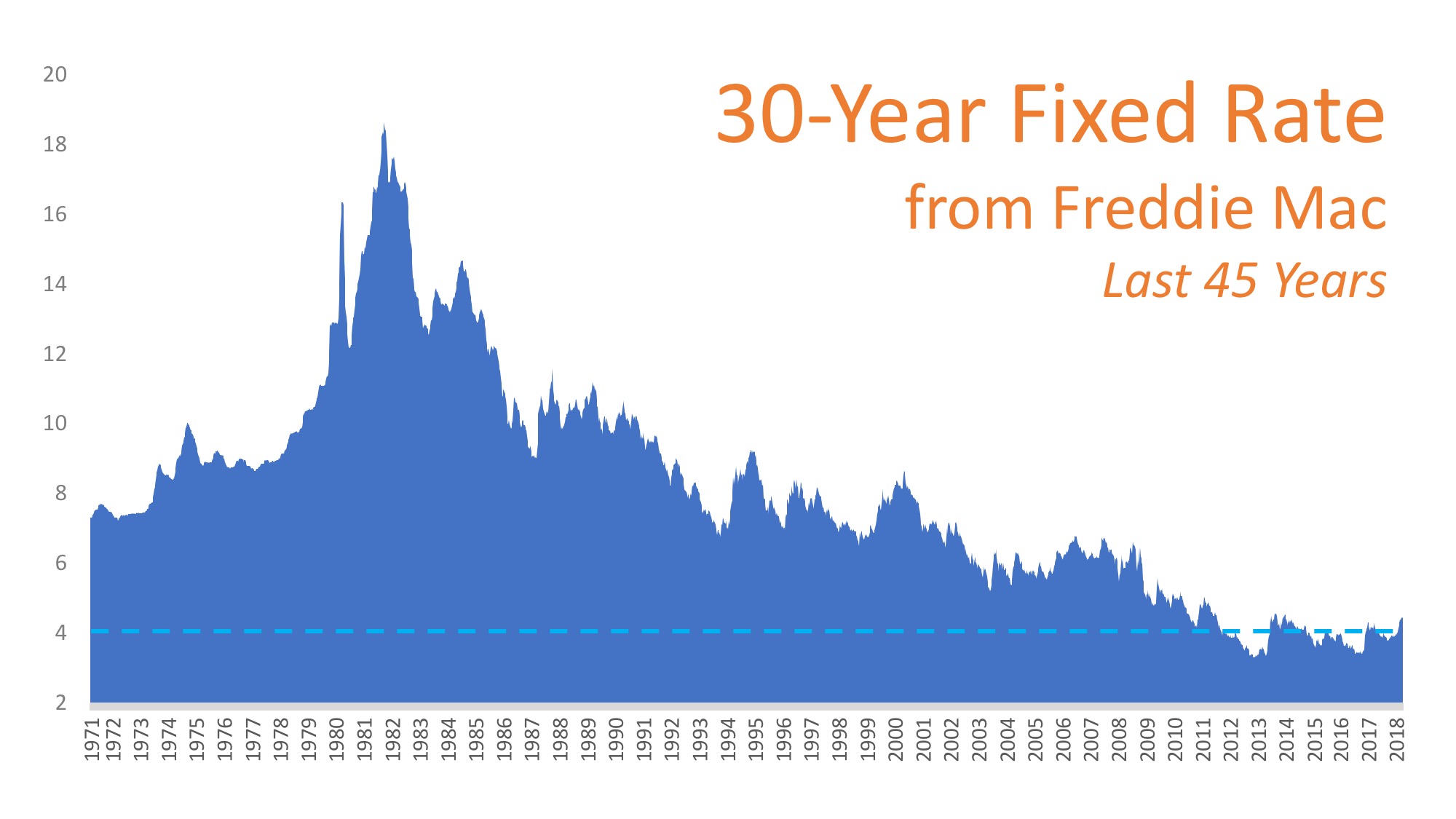

Interest rates hovered around 4% for the majority of 2017, which gave many buyers relief from rising home prices and helped with affordability. In the first quarter of 2018, rates have increased from 3.95% up to 4.45% and experts predict that rates will increase even more by the end of the year.

The rate you secure greatly impacts your monthly mortgage payment and the amount you will ultimately pay for your home. Don’t let the prediction that rates will increase stop you from purchasing your dream home this year.

Let’s take a look at a historical view of interest rates over the last 45 years. |

Last week, we shared “7 Factors To Consider When Choosing A Home To Retire In.” For some homeowners, these seven factors can be taken into account with a home renovation, but is it worth it to remodel or change floor plans?

Let’s look at this example.

Let’s say you have a 4-bedroom colonial style home in a great school district. The neighborhood is amazing, and you are very comfortable there, but your kids are all grown up and the original benefits of the home no longer apply.

You’ve always wanted a huge master suite and are considering merging 3 of the smaller bedrooms on the second floor to achieve this dream.

In the short term, you are over the moon excited about your newly renovated oasis.

In the long term, when you go to sell your home down the road, you’ve now taken a 4-bedroom home in a great school district and turned it into a 2-bedroom home. Your pool of potential buyers has shrunk significantly and so has the value of your home (unless you are able to find someone who has the exact needs you have today!).

Why not consider listing your 4-bedroom home now and moving into a gorgeous 2-bedroom with a master suite? Your house can become a home for the next family looking for that perfect neighborhood with a great school district to raise their kids in!

You may even be able to achieve your dream in the same area you love, without having to give up your favorite restaurants and grocery stores.

Bottom Line

If you are debating a major renovation that would change the layout of your home, before you pick up that sledgehammer, let’s get together and discuss the available listings in our area that might meet your needs today!

|